CYBERBANK CORE

Escalabilidade pronta para o futuro do seu banco.

Modernize suas operações bancárias com o Cyberbank Core — uma plataforma nativa da nuvem de última geração, projetada para acelerar a inovação, melhorar a experiência do cliente e aumentar a eficiência operacional.

BANCO CENTRAL DE ÚLTIMA GERAÇÃO

Solução bancária full-stack de Geração 3.0 quando combinada com Digital.

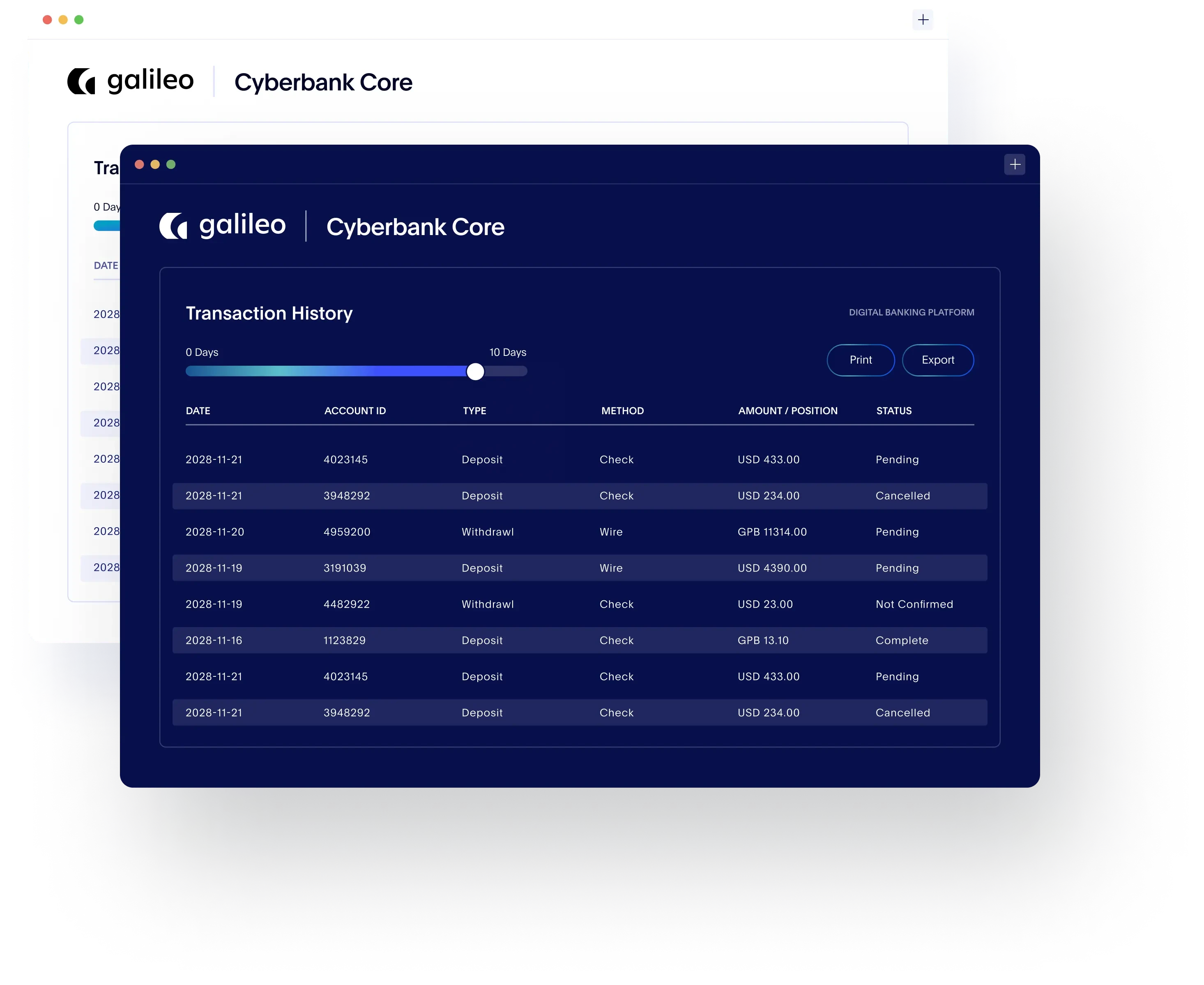

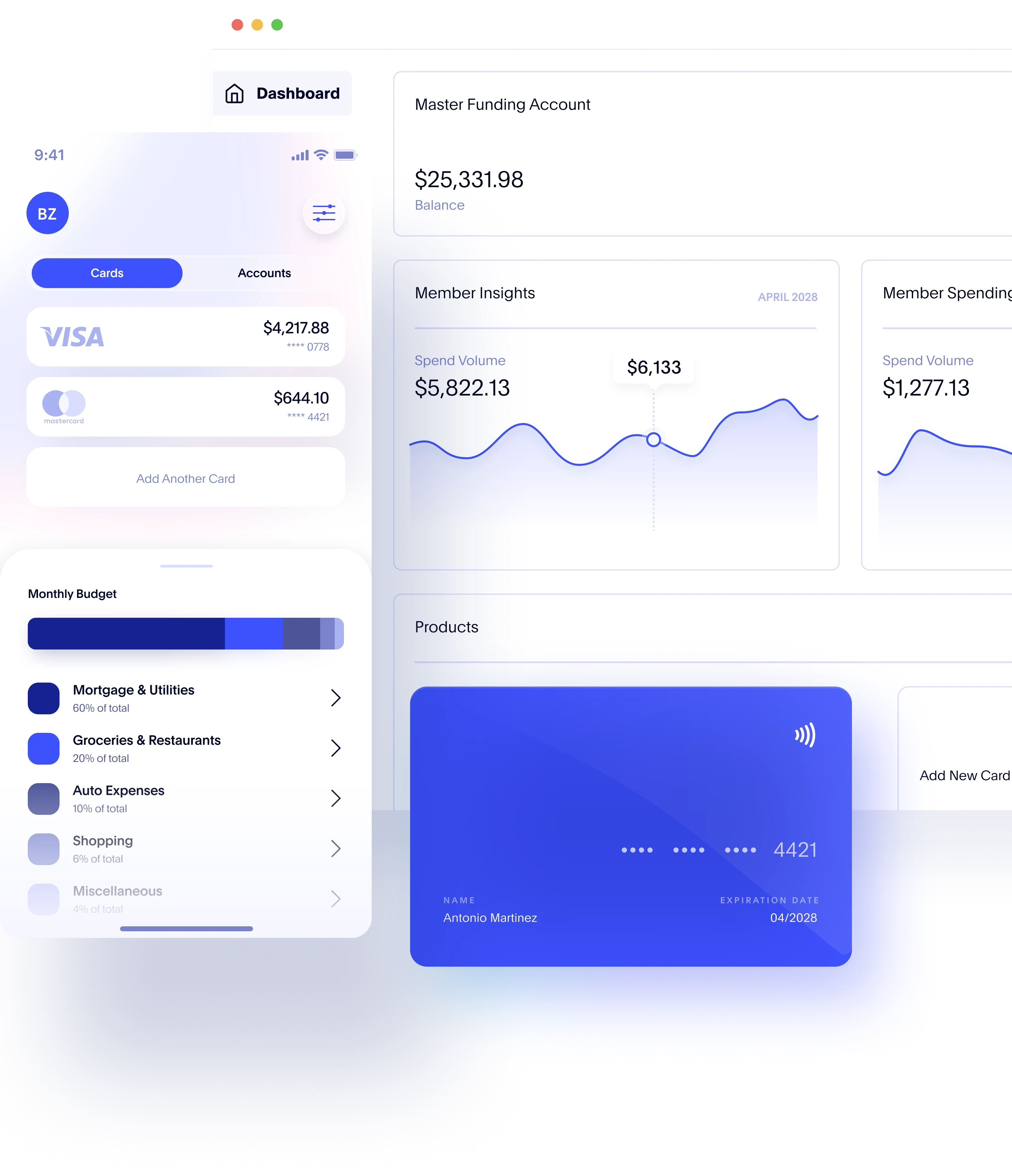

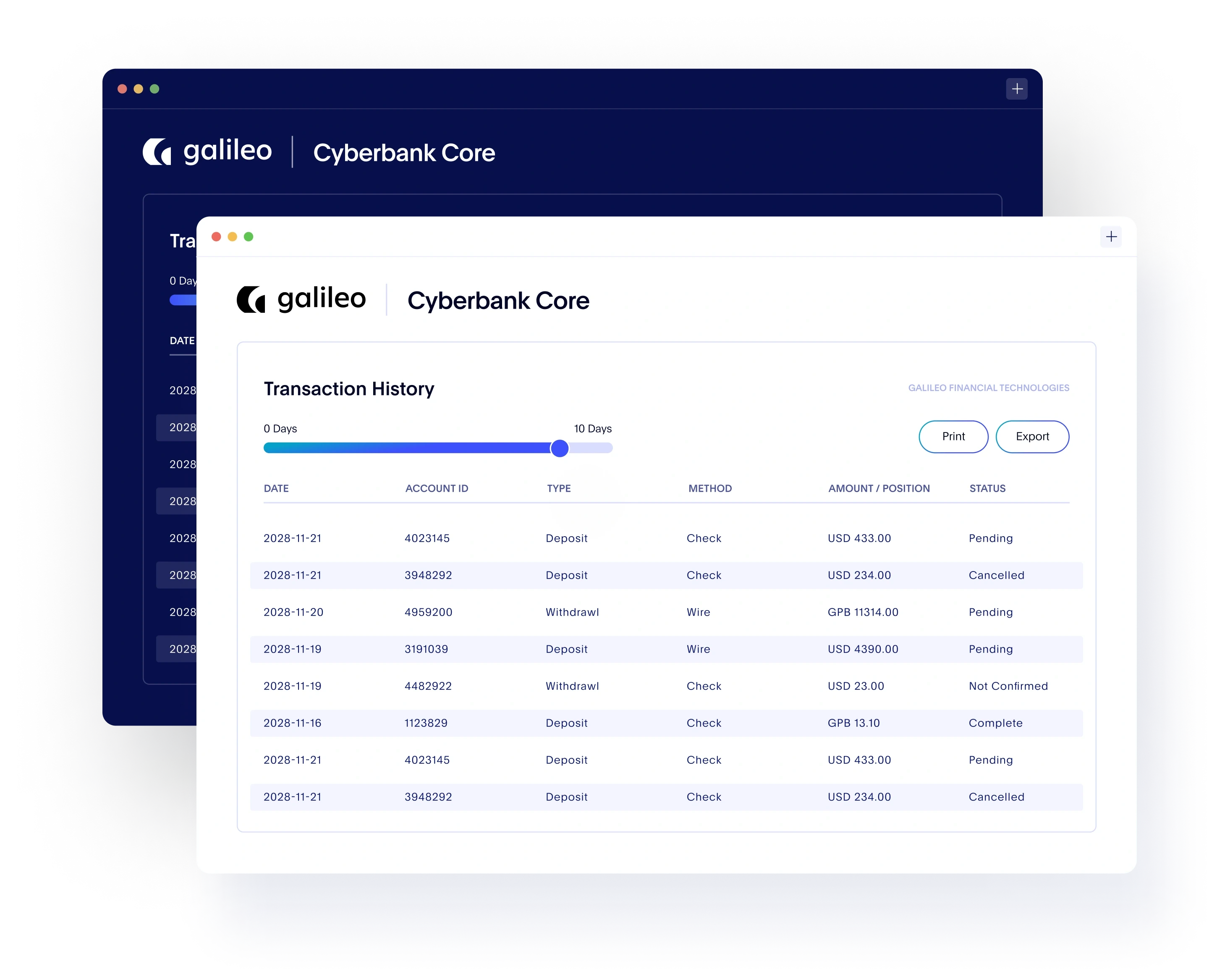

O Cyberbank Core é uma plataforma de core bancário moderna e API-first, criada para permitir que instituições financeiras e bancos ofereçam soluções financeiras inovadoras e centradas no cliente. Concebido para escalabilidade, flexibilidade e integração rápida, o Cyberbank Core reúne depósitos, empréstimos e serviços de pagamento para substituir sistemas legados, podendo escalar para mais de 10 000 transações por segundo sem comprometer o desempenho.

Capacitando os bancos a inovar com mais rapidez, integração perfeita e expansão sem esforço.

O Problema do "Core"

Os sistemas centrais tradicionais frequentemente enfrentam limitações como falta de agilidade, altos custos operacionais e desafios na integração com tecnologias emergentes ou soluções de terceiros.

Produtos Personalizados

Cyberbank Core resolve esses problemas fornecendo uma plataforma modular baseada em APIs, que simplifica operações, aprimora a inovação de produtos e proporciona experiências fluidas aos clientes.

A Solução

Ao substituir sistemas legados rígidos, o Cyberbank Core permite que os bancos lancem rapidamente novos produtos financeiros, ampliem operações e se integrem perfeitamente a ecossistemas de terceiros, garantindo competitividade no cenário financeiro, sempre em evolução.

Saiba mais sobre Cyberbank Core.

.avif?u=https%3A%2F%2Fimages.ctfassets.net%2Fbvz14004tu0h%2F1VhxM2exKd5xJSst9ytkTi%2Fae125ef7d62d11d9e1b4f2e230433d98%2FSoFi_to_Adopt_Galileo-s_Cyberbank_Core_for_Sponsor_Banking__1_.png&a=w%3D1200%26h%3D675%26fm%3Davif%26q%3D75&cd=2024-10-15T19%3A26%3A16.159Z)

O Futuro do Banco

Construa o futuro do banco com Cyberbank Core.

Ajudamos você a oferecer experiências financeiras inovadoras, personalizadas e integradas que seus clientes vão adorar.